In its interim budget for 2009-10 the Union Government has allocated Rs. 1,41,703 crores for the country’ Defence Services that include three Armed Forces (i.e., the Army, the Navy and the Air Force), and other Departments, primarily Defence Research and Development Organisation (DRDO) and Defence Ordnance Factories. This is apart from Rs. 24,960 crores which have been earmarked to defray civil expenditures of Ministry of Defence (MoD) and its affiliated organisations, including, the Coast Guard, and for defence pension (Rs. 21,790 crores). In other words, the total resource available for the MoD and its various establishments is Rs. 1,66,663 crores. By convention, only budgetary provisions for the Defence Services constitute India’s defence budget.

Though the allocations made in the interim budget are not binding for the next government to follow, it is unlikely that the new government will make any major changes in the allocation, given the mandatory increases in certain components of the defence budget, the worsening security situation in the country’s neighbourhood and the gap in the country’s defence preparedness. This commentary examines the various components of the defence budget, analyses the impact of the budget on the modernisation requirements of the Armed Forces, and the problem of under-utilisation of resources under the capital head.

Vital Components

The defence budget for 2009-10 has increased by 34.19 per cent over the previous year’s budget estimate (BE) of Rs. 1,05,600 crores. However, BE of 2008-09 has been scaled upward by 8.52 per cent (Rs. 9,000 crores) to Rs. 1,14,600 crores at the revised estimate (RE) stage. This means, this year’s allocations has increased by 23.65 per cent over the RE of 2008-09. Of the total defence budget, revenue expenditure, which caters to the ‘running’ or ‘operating’ expenditure of the three Services and other departments, is pegged at Rs. 86,879 crores. Capital expenditure, which mostly caters for modernisation requirements, accounts for Rs. 54,824 crores. Of these two, revenue expenditure has been increased - in comparison to its last year’s growth of less than 7 per cent - at a much faster rate of 50.85 per cent (Rs. 29, 286 crores). The growth of capital expenditure has however declined, over the previous year’s growth, to 14.20 per cent (Rs. 6,817 crores). The sharp rise in revenue expenditure has taken its share in the defence budget to 61.31 per cent, from 54.54 per cent a year before. In other words, the share of capital expenditure has gone down by nearly 7 percentage points in these two years (see Table).

Table: Key Statistics of Defence Budgets, 2008-09 and 2009-10 2008-09 2009-10

2008-09

2009-10

Defence Budget (Rs. in crores)

1,05,600

1,41,703

Growth of Defence Budget (%)

10.00

34.19

Revenue Expenditure (Rs in crores)

57,593

86,879

Share of Revenue Expenditure in Defence Budget (%)

54.54

61.31

Growth of Revenue Expenditure (%)

6.50

50.85

Capital Expenditure (Rs. in crores)

48,007

54,824

Share of Capital Expenditure in Defence Budget (%)

45.46

38.69

Growth of Capital Expenditure (%)

14.51

14.20

The faster growth of revenue expenditure is primarily due to the hefty increase in pay and allowances flowing from the implementation of Sixth Central Pay Commission (CPC). To put the figure in perspective, total budgeted pay and allowances debited from the Services’ budgets has more than doubled from 21,891.67 crores in 2008-09 to Rs. 44,500.69 crores in 2009-10.

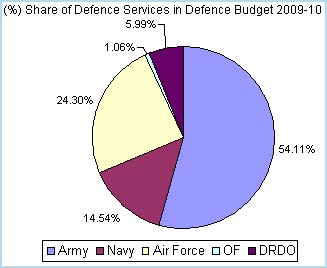

Service-wise, the Army accounts for the largest share of the 2009-10 budget with an approximate allocation of Rs. 76,680 crores, followed by the Air Force (Rs. 34,432 crores) and the Navy (Rs. 20,604 crores). While the Ordnance Factories (OF) have a budget of Rs.1,505.45 crores, the DRDO’s budget is Rs. 8,481.54 crores (see Figure-1 for percentage share of Defence Services).

Figure-I

Impact on Modernisation

The Indian Armed Forces are on a modernisation drive. The shopping list of the Services includes virtually all types of weapons and systems, including big-guns, fighter aircrafts, armoured vehicles, radars, missiles, naval vessels, among others. The most pertinent question is whether the latest budget makes necessary provisions to meet these requirements. Given the fact that the modernisation programme of the armed forces largely depends on capital acquisitions, it boils down to how capital budget is allocated.

Assuming that nearly 80 per cent of the capital budget is meant for capital acquisitions, the latter consisting of 60 per cent of committed liabilities and 40 per cent of new schemes, the main sub-divisions of the capital budget are as below:

Total Capital Budget: Rs. 54,824 crores

Capital Acquisition: Rs. 43,859 crores

Committed Liabilities: Rs.26,316 crores

New Schemes: Rs.17,544 crores

From the above, it is evident that a substantial amount will be available for capital procurement. Moreover, over Rs. 17,500 crores (nearly 30 per cent of the capital budget) will be available for new weapons and systems that the Armed Forces have planned for induction. While this augurs well from the modernisation point of view, much depends on how much and how the resources are spent in the coming fiscal.

Higher Allocation and Under-utilisation of Resources

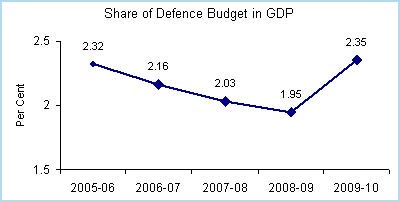

The growth of over 34 per cent in India’s defence budget is one of the highest in the country’s history of defence spending (the last time the defence budget was increased by over 30 per cent was in 1987-88 when allocation was increased by 43.4 per cent to Rs. 12,512 cores). In the recent past, the defence budget, despite registering modest growth rates, has been subjected to criticism in view of its declining shares in total central government expenditure and gross domestic product. In fact, the defence budget had decreased to below two per cent of GDP in the last fiscal year (see Figure-II). The new budget, defying all criticism, has made a substantial increase in allocations. From the perspective of resources allocation, the defence budget for 2009-10 represents 14.87 per cent of total central government expenditure, and 2.35 per cent of gross domestic product (GDP). The corresponding figures for 2008-09 are 14.06 per cent and 1.95 per cent respectively.

Figure-II

However, accompanying the growth in defence budget is the problem of utilisation of resources under the capital head. As the latest budget reveals, the budgeted capital expenditure for 2008-09 has decreased by Rs. 7,007 crores (15 per cent) from Rs. 48, 007 crores to Rs. 41,000 crores at the RE stage. Its implication is also seen in the wide variation in the growth of the capital budget. If the defence establishments had fully spent the entire 2008-09 capital budget, the 2009-10 capital expenditure would have seen only 14.2 per cent growth instead of 33.72 per cent rise (Rs. 13,824 crores) that has been registered over the previous year’s RE.

It is ironical that while capital expenditure has been increased substantially over the years, not sufficient attention has been devoted to spending those resources in a time-bound manner. As a result, under-utilisation of resources has increased with the growth in each year’s capital expenditure. In absolute number, under-utilisation has increased by over four-and-a-half times between 2004-05 and 2008-09. In percentage terms, it has increased from 4 per cent to 15 per cent in the same period (see Figure-III).

Figure-III

As the defence preparedness of the country largely depends on the firepower it possess, which in turn depends on capital expenditure, the latter’s timely and efficient utilisation deserves due consideration. Though MoD in recent years has tried to improve acquisition procedure, it appears inadequate to expedite the process. The recurring underutilisation of resources is a case in point to seriously examine the weakness in the system. If necessary a complete overhaul of the acquisition system may be considered to ensure that funds are utilised in a proper time frame and for the purpose it is envisaged for.

Conclusion

India’s defence budget 2009-10 has no doubt registered an impressive growth of over 34 per cent. However, much of the growth is accounted for by the increase in revenue expenditure, which, in turn, has been inflated by the surge in pay and allowances necessitated by the implementation of the recommendations of the Sixth Pay Commission. The impact of the increased provision for pay and allowances is such that the revenue budget’s share in the defence budget has increased to more than 61 per cent, compared to its previous year’s share of less than 55 per cent. The consequent decrease in the share of capital expenditure has resulted in its modest 14.2 per cent growth amounting to an additional provision of Rs. 6,817 crores over last year’s allocations. Nonetheless, the allocation of Rs. 54,824 crores under the capital head is still substantial in absolute terms. Considering that around 80 per cent of the capital budget would be available for procurement of weapons and systems, including some new ones, the defence establishment would be under pressure to spend the resources in a time-bound manner. Experience in the recent past shows that under-utilisation of capital budget has increased with each year’s allocations. This necessitates a critical examination of the acquisition system to ensure that the Armed Forces are equipped with the right equipment at the right time.

India’s Defence Budget 2009-10: An Assessment

More from the author

In its interim budget for 2009-10 the Union Government has allocated Rs. 1,41,703 crores for the country’ Defence Services that include three Armed Forces (i.e., the Army, the Navy and the Air Force), and other Departments, primarily Defence Research and Development Organisation (DRDO) and Defence Ordnance Factories. This is apart from Rs. 24,960 crores which have been earmarked to defray civil expenditures of Ministry of Defence (MoD) and its affiliated organisations, including, the Coast Guard, and for defence pension (Rs. 21,790 crores). In other words, the total resource available for the MoD and its various establishments is Rs. 1,66,663 crores. By convention, only budgetary provisions for the Defence Services constitute India’s defence budget.

Though the allocations made in the interim budget are not binding for the next government to follow, it is unlikely that the new government will make any major changes in the allocation, given the mandatory increases in certain components of the defence budget, the worsening security situation in the country’s neighbourhood and the gap in the country’s defence preparedness. This commentary examines the various components of the defence budget, analyses the impact of the budget on the modernisation requirements of the Armed Forces, and the problem of under-utilisation of resources under the capital head.

Vital Components

The defence budget for 2009-10 has increased by 34.19 per cent over the previous year’s budget estimate (BE) of Rs. 1,05,600 crores. However, BE of 2008-09 has been scaled upward by 8.52 per cent (Rs. 9,000 crores) to Rs. 1,14,600 crores at the revised estimate (RE) stage. This means, this year’s allocations has increased by 23.65 per cent over the RE of 2008-09. Of the total defence budget, revenue expenditure, which caters to the ‘running’ or ‘operating’ expenditure of the three Services and other departments, is pegged at Rs. 86,879 crores. Capital expenditure, which mostly caters for modernisation requirements, accounts for Rs. 54,824 crores. Of these two, revenue expenditure has been increased - in comparison to its last year’s growth of less than 7 per cent - at a much faster rate of 50.85 per cent (Rs. 29, 286 crores). The growth of capital expenditure has however declined, over the previous year’s growth, to 14.20 per cent (Rs. 6,817 crores). The sharp rise in revenue expenditure has taken its share in the defence budget to 61.31 per cent, from 54.54 per cent a year before. In other words, the share of capital expenditure has gone down by nearly 7 percentage points in these two years (see Table).

Table: Key Statistics of Defence Budgets, 2008-09 and 2009-10 2008-09 2009-10

The faster growth of revenue expenditure is primarily due to the hefty increase in pay and allowances flowing from the implementation of Sixth Central Pay Commission (CPC). To put the figure in perspective, total budgeted pay and allowances debited from the Services’ budgets has more than doubled from 21,891.67 crores in 2008-09 to Rs. 44,500.69 crores in 2009-10.

Service-wise, the Army accounts for the largest share of the 2009-10 budget with an approximate allocation of Rs. 76,680 crores, followed by the Air Force (Rs. 34,432 crores) and the Navy (Rs. 20,604 crores). While the Ordnance Factories (OF) have a budget of Rs.1,505.45 crores, the DRDO’s budget is Rs. 8,481.54 crores (see Figure-1 for percentage share of Defence Services).

Figure-I

Impact on Modernisation

The Indian Armed Forces are on a modernisation drive. The shopping list of the Services includes virtually all types of weapons and systems, including big-guns, fighter aircrafts, armoured vehicles, radars, missiles, naval vessels, among others. The most pertinent question is whether the latest budget makes necessary provisions to meet these requirements. Given the fact that the modernisation programme of the armed forces largely depends on capital acquisitions, it boils down to how capital budget is allocated.

Assuming that nearly 80 per cent of the capital budget is meant for capital acquisitions, the latter consisting of 60 per cent of committed liabilities and 40 per cent of new schemes, the main sub-divisions of the capital budget are as below:

From the above, it is evident that a substantial amount will be available for capital procurement. Moreover, over Rs. 17,500 crores (nearly 30 per cent of the capital budget) will be available for new weapons and systems that the Armed Forces have planned for induction. While this augurs well from the modernisation point of view, much depends on how much and how the resources are spent in the coming fiscal.

Higher Allocation and Under-utilisation of Resources

The growth of over 34 per cent in India’s defence budget is one of the highest in the country’s history of defence spending (the last time the defence budget was increased by over 30 per cent was in 1987-88 when allocation was increased by 43.4 per cent to Rs. 12,512 cores). In the recent past, the defence budget, despite registering modest growth rates, has been subjected to criticism in view of its declining shares in total central government expenditure and gross domestic product. In fact, the defence budget had decreased to below two per cent of GDP in the last fiscal year (see Figure-II). The new budget, defying all criticism, has made a substantial increase in allocations. From the perspective of resources allocation, the defence budget for 2009-10 represents 14.87 per cent of total central government expenditure, and 2.35 per cent of gross domestic product (GDP). The corresponding figures for 2008-09 are 14.06 per cent and 1.95 per cent respectively.

Figure-II

However, accompanying the growth in defence budget is the problem of utilisation of resources under the capital head. As the latest budget reveals, the budgeted capital expenditure for 2008-09 has decreased by Rs. 7,007 crores (15 per cent) from Rs. 48, 007 crores to Rs. 41,000 crores at the RE stage. Its implication is also seen in the wide variation in the growth of the capital budget. If the defence establishments had fully spent the entire 2008-09 capital budget, the 2009-10 capital expenditure would have seen only 14.2 per cent growth instead of 33.72 per cent rise (Rs. 13,824 crores) that has been registered over the previous year’s RE.

It is ironical that while capital expenditure has been increased substantially over the years, not sufficient attention has been devoted to spending those resources in a time-bound manner. As a result, under-utilisation of resources has increased with the growth in each year’s capital expenditure. In absolute number, under-utilisation has increased by over four-and-a-half times between 2004-05 and 2008-09. In percentage terms, it has increased from 4 per cent to 15 per cent in the same period (see Figure-III).

Figure-III

As the defence preparedness of the country largely depends on the firepower it possess, which in turn depends on capital expenditure, the latter’s timely and efficient utilisation deserves due consideration. Though MoD in recent years has tried to improve acquisition procedure, it appears inadequate to expedite the process. The recurring underutilisation of resources is a case in point to seriously examine the weakness in the system. If necessary a complete overhaul of the acquisition system may be considered to ensure that funds are utilised in a proper time frame and for the purpose it is envisaged for.

Conclusion

India’s defence budget 2009-10 has no doubt registered an impressive growth of over 34 per cent. However, much of the growth is accounted for by the increase in revenue expenditure, which, in turn, has been inflated by the surge in pay and allowances necessitated by the implementation of the recommendations of the Sixth Pay Commission. The impact of the increased provision for pay and allowances is such that the revenue budget’s share in the defence budget has increased to more than 61 per cent, compared to its previous year’s share of less than 55 per cent. The consequent decrease in the share of capital expenditure has resulted in its modest 14.2 per cent growth amounting to an additional provision of Rs. 6,817 crores over last year’s allocations. Nonetheless, the allocation of Rs. 54,824 crores under the capital head is still substantial in absolute terms. Considering that around 80 per cent of the capital budget would be available for procurement of weapons and systems, including some new ones, the defence establishment would be under pressure to spend the resources in a time-bound manner. Experience in the recent past shows that under-utilisation of capital budget has increased with each year’s allocations. This necessitates a critical examination of the acquisition system to ensure that the Armed Forces are equipped with the right equipment at the right time.

Related Publications